The Quiet Cost of the Paycheck: Understanding Income Taxes, Payroll Taxes, and the Regressive Tax Debate

Every payday, millions of Americans look at their paycheck and ask the same question: “Where did all my money go?”

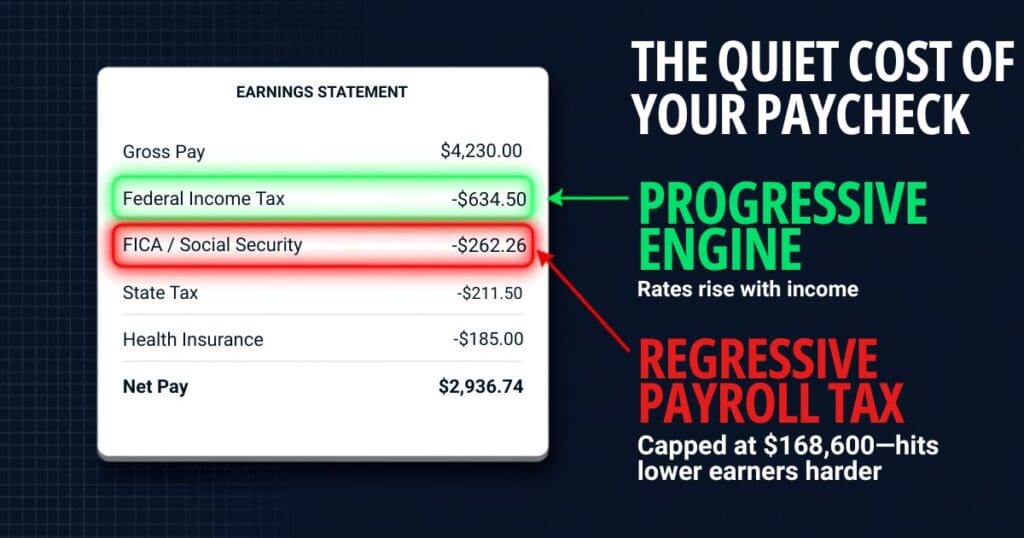

Most people know about federal income taxes, but far fewer realize how the balance of a standard payroll tax vs income tax shapes their net pay. While political debates heavily emphasize Progressive Taxes versus Flat Taxes, analyzing a payroll tax vs income tax dynamic reveals a hidden, highly debated concept that receives far less mainstream attention: the Regressive Tax. To understand why fiscal policy directly impacts your financial leverage, we must look at how these two completely different tax systems function on nearly every American paycheck.

To understand why this matters, we need to look at two completely different tax systems that appear on nearly every American paycheck.

The Framework: Income Tax vs. Payroll Tax

Although both deductions come out of your paycheck, they serve entirely different societal purposes and operate under vastly different mathematical rules. Check out out tax series.

1. Income Tax: The Progressive Engine

Federal income taxes help fund a wide range of general government services, including national defense, infrastructure projects, federal courts, and everyday government operations.

The federal income tax is structurally progressive, meaning tax rates increase as an individual’s income rises. In a progressive system, higher earners pay a larger percentage of their income in taxes than lower earners. The underlying philosophy is called the ability-to-pay principle—the idea that those with greater financial resources should contribute a larger share to maintain the society that facilitated their success.

2. Payroll Tax: The Social Insurance System

Payroll taxes, commonly known as FICA taxes (Federal Insurance Contributions Act), fund dedicated social safety nets: Social Security and Medicare.

Unlike the income tax, the payroll tax burden is split evenly between the worker and the employer. For the worker’s portion, every employee sees a direct deduction of:

- 6.2% for Social Security

- 1.45% for Medicare

At first glance, payroll taxes appear to be a textbook flat tax because everyone faces the exact same percentage on paper. However, one critical legislative rule completely flips the math.

How the Social Security Cap Changes the Equation

In 2026, Social Security taxes apply only to the first $184,500 of earned income. This is known as the Social Security wage base limit.

Once a worker earns more than that amount, the 6.2% Social Security tax drops to 0% for the remainder of the year. While the 1.45% Medicare tax continues indefinitely, the Social Security portion completely halts.

This creates a stark divergence: lower- and middle-income workers pay the full Social Security tax rate on every single dollar they earn, while high earners eventually stop paying it altogether. Because the tax consumes a smaller total percentage of a wealthy person’s income than a middle-class person’s income, economists classify the Social Security payroll tax as a Regressive Tax.

Politics 101 Takeaway

- Progressive Tax: The tax rate increases as income increases (e.g., Federal Income Tax).

- Flat Tax: Everyone pays the exact same percentage, regardless of income.

- Regressive Tax: The effective tax rate decreases as income increases, leaving lower earners to pay a larger share of their total income than high earners.

The Tale of Three Houses

To see how these tax structures interact in the real world, imagine three neighbors living on the same street.

House A: Marcus, the Middle-Class Manager

Marcus manages a regional logistics hub and earns $95,000 per year. Because his income remains safely below the $184,500 wage cap, he pays the full 6.2% payroll tax on 100% of his earnings throughout the entire year. Every single paycheck receives the exact same deduction. The money removed from his paycheck is liquid capital that cannot be used for emergency savings, home repairs, or family medical expenses.

House B: Sophia, the High Earner

Sophia is a senior software architect earning $250,000 per year. Like Marcus, she pays her full payroll taxes at the beginning of the year. However, once her year-to-date earnings clear the $184,500 threshold (typically around mid-autumn), the 6.2% Social Security tax completely disappears from her remaining paychecks. Her top $65,500 of income is completely exempt from the tax. As a result, the payroll tax consumes a much smaller percentage of her overall annual income than it does for Marcus.

House C: The Real-Life Impact of Cash Reserves

Tax policy often sounds abstract until it intersects with a sudden family crisis. A hard-working friend of mine in Texas spent years paying both his payroll and income taxes while raising a family. When both of his parents became seriously ill, he assumed—like many Americans—that the safety-net systems he had faithfully funded via FICA would step in with significant institutional support.

Instead, he discovered a wall of bureaucratic gaps, and the financial burden fell squarely back on his family. Because the regressive nature of everyday payroll deductions takes a primary bite out of working-class paychecks from dollar one, families have less of a liquid cash cushion to save themselves when tragedy hits. To survive, he had to make the agonizing choice to scale back his father’s medical treatments to a baseline package they could physically afford out-of-pocket.

The Paycheck Breakdown

When you map out the dual-system structure across income classes, the real-world impact becomes perfectly clear:

| Taxpayer | Annual Income | Income Tax Structure | Payroll Tax Structure | Practical Paycheck Impact | Effective SS Rate |

|---|---|---|---|---|---|

| Working-Class | $45,000 | Progressive; shielded by lower entry brackets. | Regressive; applies to 100% of earnings. | Less room to build up vital emergency savings. | 6.2% |

| Marcus (Middle Class) | $95,000 | Progressive; faces a moderate, balanced tax burden. | Regressive; applies to 100% of earnings. | Bears the full, uncaped percentage all year long. | 6.2% |

| Sophia (High Earner) | $250,000 | Progressive; top dollars hit higher tax brackets. | Regressive; Social Security tax halts at wage cap. | Paycheck receives a net increase late in the year. | ~4.5%* |

Why People Disagree: The Ideological Debate

Like almost all fiscal policy in political science, reasonable people look at these exact same mathematical facts and arrive at polar opposite philosophical conclusions.

The Argument for the Current System (The Conservative Perspective)

Supporters of the wage cap point out that Social Security benefits are strictly capped at retirement. Their reasoning is rooted in procedural fairness: if the government limits the maximum payout a person can receive in their old age, it is only fair to limit their contributions on the way in. Under this classical view, Social Security is structured like a mutual insurance program, not an open-ended wealth redistribution system.

The Argument for Reform (The Progressive Perspective)

Critics argue that capping the tax creates an unfair, upside-down burden on the working and middle classes. They believe high earners should continue paying the 6.2% tax on every dollar they make, just like Marcus does. Proponents of “scraping the cap” argue this reform would instantly stabilize Social Security’s long-term insolvency issues while providing robust funding to expand social programs for vulnerable families in crisis.

What This Means for You

The next time you open your paycheck, take a closer look at the line-item deductions. You will see that what we casually call “taxes” is actually a complex web of competing economic philosophies operating under entirely different rules.

Understanding these mechanisms explains why fiscal policy remains the ultimate battleground of American politics. The question isn’t simply a matter of accounting. The deeper political question is: Who should pay what share—and why?

Join the Discussion

Do you believe the Social Security wage cap is a fair, structural limit within a capped-benefit system? Or do you think removing the cap is necessary to create an equitable distribution of the national tax burden?

Drop your thoughts in the comments below!

Further Reading & Sources

Foundational Books

- The Flat Tax / Free Market Perspective: Capitalism and Freedom by Milton Friedman (1962). A classic defense of competitive capitalism and a foundational argument for structural tax simplification.

- The Ability-to-Pay Perspective: The Wealth of Nations by Adam Smith (1776). Though hailed as the pioneer of free markets, Smith explicitly argued that citizens should contribute to the state in direct proportion to their financial abilities.

- The Modern Equity Debate: The Triumph of Injustice: How the Rich Dodge Taxes and How to Make Them Pay by Emmanuel Saez and Gabriel Zucman (2019). A rigorous modern look at how macroeconomic tax burdens have shifted across income groups over the last century.

Data & Policy Resources

- Tax Foundation (taxfoundation.org): An independent, nonpartisan research organization providing historical breakdowns of federal and state tax brackets.

- Center on Budget and Policy Priorities (cbpp.org): A policy institute analyzing how federal budget changes specifically alter the financial landscapes of low-to-middle-income households.

- Social Security Administration (ssa.gov): The official federal repository detailing current tax rates, historical wage limits, and benefit calculation metrics.